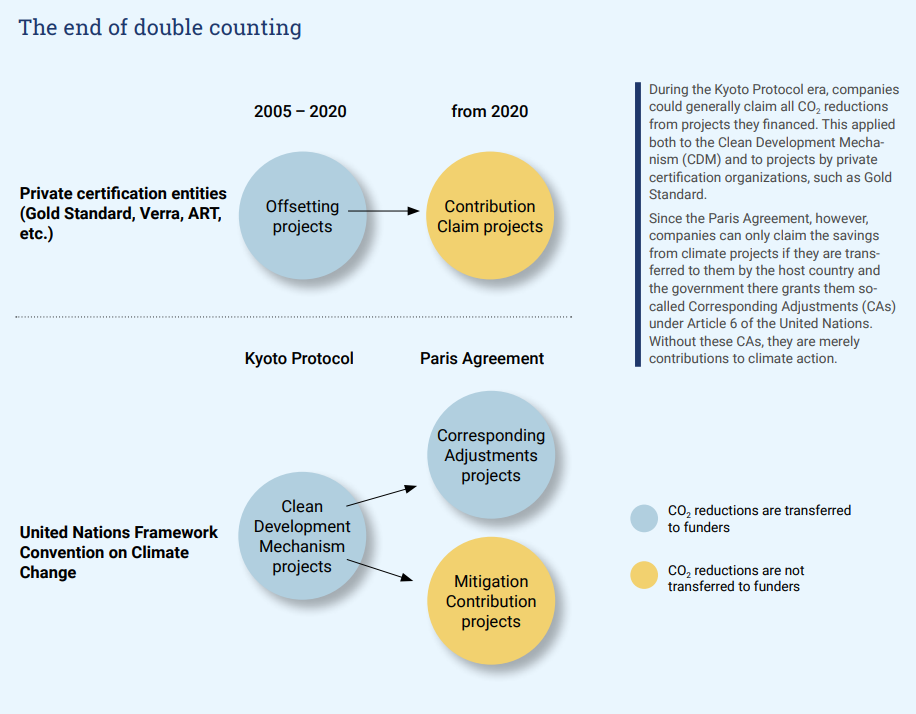

There’s a lot happening in the market for certified carbon reductions: New regulations aim to improve the quality of climate projects. This is policymakers’ response to recent criticism. But will all carbon offset providers, and their customers get on board? Or will some look for loopholes, as has often been the case? Here’s what we expect.

The first day hadn’t even passed – and the gavel came down in Baku: On November 11, signatories to the Paris Agreement voted for new rules on Carbon offsetting. This is unusual, given that climate conferences aren’t exactly known for quick decisions. Although the Paris Agreement entered into force in 2020, concrete rules for the Article 6 mechanism are only now being established. They stipulate how governments and private organisations in the Global North can support the Global South in Climate action. The new rules under the Paris Agreement are necessary because countries in the Global South are now subject to climate targets, known as Nationally Determined Contributions (NDCs). These carry more weight than the previous reporting obligations under the Kyoto Protocol. All climate measures within a country are first recorded in that state’s emissions inventory. If a foreign-funded climate project Claims these CO₂ reductions for itself, double counting can occur. Therefore, a climate organization from abroad should ensure that the host country of the climate project does not credit the savings toward its own NDCs.

More Climate Action Through Corresponding Adjustments

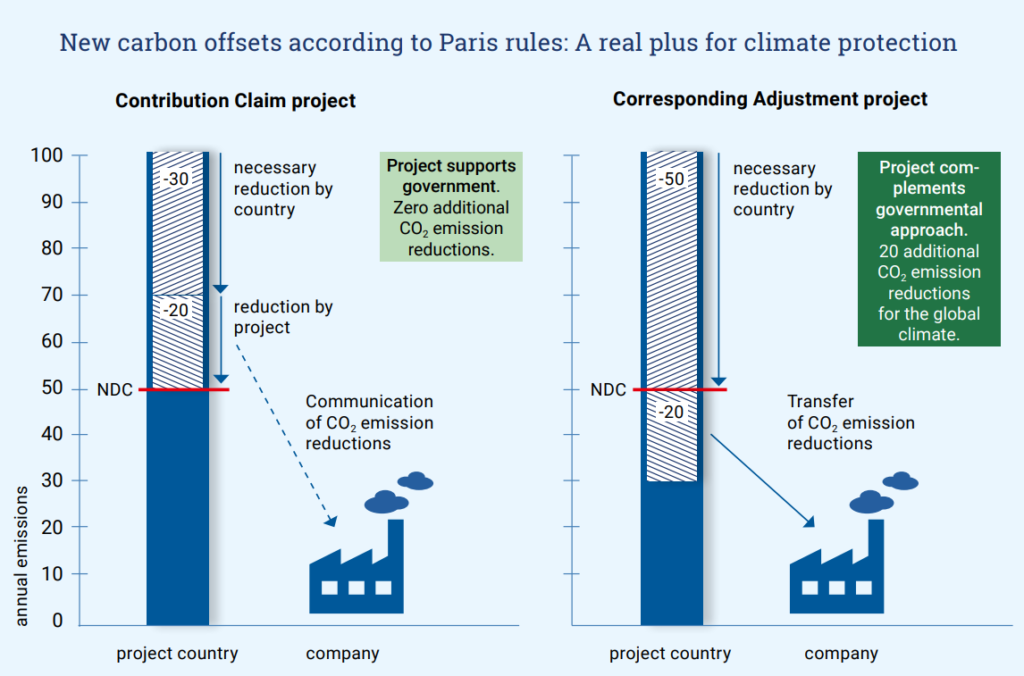

These adjustments in carbon accounting are called “Corresponding Adjustments” (CAs). Here, states where climate projects take place remove the CO₂ savings from their own greenhouse gas balance sheet. This allows funders to claim them for themselves. However, host countries don’t give up their CO₂ savings easily – after all, they could use them for their own climate targets. They have good reason to demand investments in technology and knowledge transfer from climate organisations in return. This is also an opportunity for climate projects to achieve higher quality. The CA negotiations between atmosfair and the Nigerian government illustrate this: We receive credits for the CO₂ savings from our efficient stoves only because we do more than just build factories with high-tech machinery. For example, we finance public wells in the Sahel region where the population can access water. We also support Nigeria in building a hydrogen industry. Thus, our Nigerian project is a win-win situation for both sides.

Such offsetting projects offer additional benefits beyond fair partnership between the Global North and South. They can expand climate action, since the savings are not credited to the respective state’s NDCs but occur in addition to government programs. While there’s no guarantee that a project with CAs will actually expand climate action, CA projects offer the best conditions for this and the greatest possible regulatory certainty. Therefore, offsetting with CAs is the ideal form of climate action when it’s not possible to avoid or reduce emissions. If companies are already willing to pay for climate action, the projects they support should bring real added value. The German Environment Ministry publicly took exactly this position at COP26 in Glasgow.

atmosfair is the only provider in Germany offering offsetting under Article 6.4, as determined by Stiftung Warentest (see Finanztest, February 19, 2025: “Fliegen, spenden und dem Klima helfen”). Without CA agreements, carbon credits merely represent contributions to climate protection, socalled Contribution Claims (CCs). Unfortunately, we are already seeing other organisations attempting to create the impression of full-fledged offsetting even without CAs. These providers exploit the fact that many people are unfamiliar with the new fundamental principles of Carbon offsetting. For example, they speak of “contributions to carbon balancing,” which falsely creates the impression of genuine offsetting. This calls not only for increased consumer education efforts but also for legal regulations governing what claims companies may make in their marketing. Even the term “offsetting” is now being used by companies despite their projects only qualifying as CCs.

Project Comparison: Contribution Claims and Corresponding Adjustments

| Contribution Claim project | Corresponding Adjustment project | |

|---|---|---|

| Who finances the climate project? | A climate organization or company from abroad | A climate organization or company from abroad |

| Who can claim the CO₂ reductions? | The host country | The project funder |

| What must the host country do to achieve its climate targets (NDC)? | It can use the project’s reductions to meet its NDC | It must achieve the NDC entirely on its own; the project’s reductions occur in addition to the government program |

| What can the project funder claim? | It has made a “contribution to climate action” (hopefully, though it could also be replacing government efforts) | It has offset its own unavoidable residual emissions |

| What do the projects bring to people in the host country? | The projects can, but don’t have to, contribute to the United Nations Sustainable Development Goals | The projects must contribute to the United Nations Sustainable Development Goals |

European Union tightens controls

To prevent misleading communication, the European Commission adopted the Green Claims Directive (GCD), which entered into force in 2024. It aims to protect consumers from misleading claims, which are particularly common in climate protection. Companies are no longer permitted to describe themselves as “climate neutral,” for example, after merely offsetting their climaterelevant emissions.

The Commission also sought to expand corporate sustainability reporting through the Corporate Sustainability Reporting Directive (CSRD). It requires companies to report extensively on their emissions and have these reports externally verified, similar to what is mandated for financial accounting. This is intended to make corporate climate action more transparent and encourage the selection of higherimpact measures. Originally, these regulations were intended to apply to approximately 50,000 large and medium-sized companies across the EU. In February 2025, however, the EU Commission significantly weakened the scope of the CSRD through the Omnibus Regulation to spare smaller companies from bureaucracy. Now only companies with more than 1,000 employees must Report extensively on their emissions and offsetting, which applies to just 6,000 firms across the entire European Union.

Private watchdogs step in

It’s not only the United Nations and the European Union currently working to improve carbon offsetting. Two independent, private institutions have also become active in this area in recent years: the Integrity Council for the Voluntary Carbon Market (ICVCM) and the Carbon Credit Quality Initiative (CCQI). These are smaller non-governmental organisations staffed by

a number of experts who critically examine both the CDM and the methods of private certification organisations like Gold Standard. At the same time, they develop more precise methods for climate protection projects to quantify their carbon reductions and certify carbon credits that meet these principles. ICVCM and CCQI continuously refine their principles based on new scientific findings and practical experience. Their progress is now feeding into the implementation of Article 6.4.

Even before COP29 in Baku, private initiatives improved methods to calculate carbon reductions more realistically. After numerous cookstove projects came under justified criticism (see Süddeutsche Zeitung, November 14, 2024: “Warum die meisten CO₂-Sparprojekte Luftnummern sind”), the Clean Cooking Alliance responded by developing the new CLEAR standard. This addresses weaknesses in the previous CDM methodology and determines the actual impact of efficient stoves based on a region’s non-renewable biomass. The greater the share of non renewable biomass, the more forest is protected by cooking devices that require less firewood. However, if sustainable forestry prevails in a region and tree populations are fundamentally less threatened, the impact of efficient stoves is correspondingly lower.

The private initiatives themselves repeatedly face criticism. In November 2024, ICVCM certified three standards for forest protection projects despite criticism that they overestimate the effect of forest protection in most countries. For this reason, the representative from Öko-Institut withdrew from ICVCM.

The carbon market between decline and boom forecasts

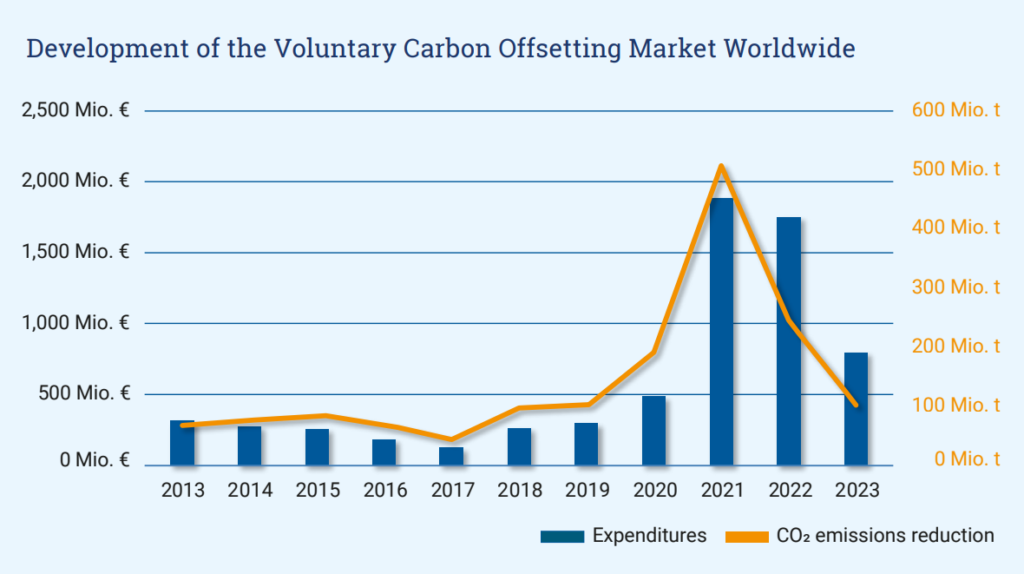

The new political framework has the potential to significantly improve the quality of private climate action. If the voluntary carbon market regains a better reputation, demand for certified carbon reductions could rise. Companies would primarily seek Climate protection projects with CAs if these are the only ones they are allowed to communicate as offsetting. However, since the price of such projects is higher, it’s also conceivable that some companies will turn away from carbon offsetting altogether.

Currently, there is no sign of a resurgence in the voluntary carbon market. In 2023, companies spent 700 million euros on carbon offsetting, significantly less than in the previous two years. In 2021 and 2022, the volume of the global carbon market (also known as the Voluntary Carbon Market, VCM) approached the two-billion-euro mark. The decline may be attributed to negative media coverage in 2023. The volume of CO₂ reductions that were certified (though not necessarily sold) in recent years also decreased over the past three years. This could be a consequence of reduced demand, but it occurred much more slowly than the decline in the volume of credits sold. A different trend emerges when looking at certified reductions that companies applied to their emissions in 2022 through 2024, meaning they “retired.” The volume of these remained nearly constant over the past three years at 180 million metric tons of CO₂ per year (MSCI Carbon Markets 2025). This suggests that companies had already stockpiled sufficient credits in previous years. Consequently, they see no Need to purchase new ones (yet). This could be another reason for the decline in market volume.

How will the market develop in the future? Despite the recent downturn, Morgan Stanley Capital International (MSCI) ventures an optimistic forecast. For 2030, it expects strong growth from the current 500 Million to 7–35 billion U.S. dollars, taking companies’ current claims at face value. The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) of the International Civil Aviation Organization (ICAO) will further boost demand for carbon offset certificates. It mandates that airlines offset a fraction of emissions from international flights. According to estimates, this could increase the volume of certified reductions by one-third (Abatable 2025). In fact, it is necessary for climate action to be increasingly financed by the private sector. Countries in the Global North are currently cutting rather than expanding their spending on development cooperation and energy transition. Moreover, climate spending in public budgets should not compete with other departments.

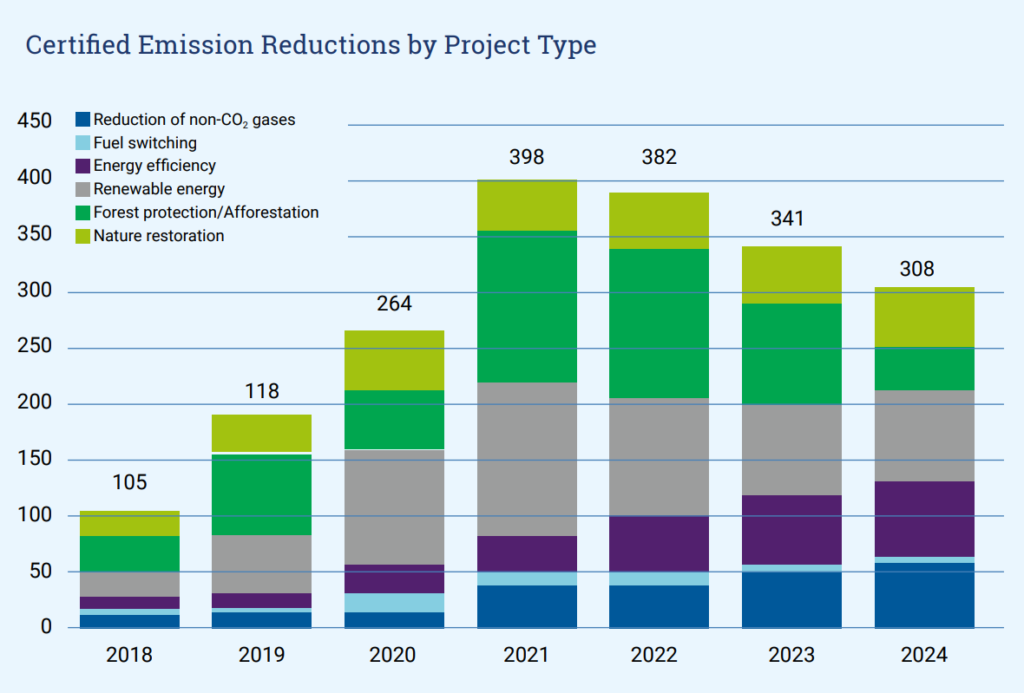

Climate Projects of the Future: More Removals, Less Forest Protection

Not much time has passed since the new offsetting rules were agreed on in November 2024. Worldwide, there are only 22 CA agreements between Climate organisations and countries, four of which atmosfair has concluded (as of 12/2024). Certified CO₂ reductions from atmosfair Projects with CA agreements accounted for 58% of our total CO₂ savings in 2024. This means we are well prepared for the new UN rules.

As for the project types themselves, a shift is clearly observable. From 2023 to 2024, the share of Projects aimed at protecting or reforesting forests (REDD+) declined by more than 50%. A number of media outlets criticized these project types most severely, which is reflected in lower demand and, with some time lag, in reduced supply. During the same period, the volume of certified CO₂ reductions from projects that protect the climate through higher energy efficiency steadily increased. These include, among others, stoves that use less firewood – like our Save 80, which we manufacture in Nigeria and Rwanda. Removal projects, which extract carbon from the atmosphere and permanently sequester it in the ground, have so far played a relatively minor role. On one hand, this can be accomplished using human-made technology, known as Direct Air Capture (DAC). On the other hand, plants can be used to draw CO₂ from the atmosphere, which occurs in our biochar projects. In 2024, we received removal credits for nearly 9,000 metric tons of CO₂ from our biochar projects. In 2025, we aim to permanently sequester 30,000 metric tons underground this way. Current developments in the voluntary Carbon market give reason to hope that the quality of climate projects is fundamentally improving: away from forest protection programs and toward negative emissions. However, there is no guarantee that carbon Offset providers will implement these projects effectively. CA agreements can, but do not automatically, lead to better projects. As is often the case, it depends on the specific design.

Share

Share